Capturing the Kingdom: Saudi Arabia’s Differentiated Strategy to Dominate the MENA Pharmaceutical Market

December 08, 2025

Saudi Arabia is executing an aggressive, capital-backed strategy to dramatically increase domestic pharmaceutical production, driven by the core tenets of Vision 2030. This initiative is a geopolitical imperative to secure national drug supply and a powerful economic engine to diversify the economy away from oil. By leveraging the immense purchasing power of its public healthcare system, the Kingdom is essentially offering a non-negotiable gateway to the Middle East’s largest pharmaceutical market, projected to exceed $15.5 billion by 2030, in exchange for mandatory local manufacturing, high-value technology transfer, and the development of specialized talent.

The Localization Drive

Saudi Arabia’s approach to capturing its domestic market is distinguished by the scale of its investments and the clarity of its policy mechanisms. The strategy targets a fundamental shift from importing nearly 70% of its medication to achieving drug security and becoming a regional manufacturing hub.

1. The Power of the Domestic Market and Procurement Mandates

Market Size: Saudi Arabia commands the biggest pharmaceutical market in the Middle East and North Africa (MENA) region. This size, fueled by a high prevalence of chronic diseases and extensive government healthcare expenditure, gives the Saudi government immense leverage over multinational companies (MNCs).

Preferential Pricing: The government, through the Saudi Food and Drug Authority (SFDA) and the General Commission for Government Procurement, has implemented preferential pricing policies and localization mandates. Locally produced pharmaceuticals often receive a significant price preference in public tenders, which constitute a large portion of the market. This creates a powerful commercial incentive for global players to partner locally or establish their own plants.

Drug Security Imperative: The localization push is explicitly linked to national security. The disruption of global supply chains, particularly during the pandemic, underscored the vulnerability of relying on foreign imports, solidifying the government’s commitment to self-sufficiency.

2. Strategic Investment as a Market Catalyst: The Role of PIF and Lifera

The Role of PIF and Lifera The Public Investment Fund (PIF), Saudi Arabia’s sovereign wealth fund, is the primary financial and strategic catalyst for localization, creating entities designed to build capacity where the private sector is hesitant.

Lifera: The CDMO Flagship launched by PIF, focused on high-value, complex biopharmaceuticals. Lifera’s mission is to rapidly build manufacturing and stockpiling capacity for essential medicines. By focusing on these critical, often patented, products, Lifera provides a ready-made platform for MNCs looking to meet localization requirements without building their own facilities from scratch. On the other hand, Lifera’s operating model is fundamentally based on forging partnerships with global companies, ensuring that the latest technology and know-how for advanced biologics are transferred directly into the Kingdom, thereby rapidly elevating the entire domestic manufacturing base.

3. Targeted Focus on High-Value and Advanced Biologics

Saudi Arabia is strategically jumping past basic generic manufacturing to target the most lucrative and future-proof segments of the pharmaceutical industry:

Biologics and Advanced Therapies — The localization targets specifically emphasize biologics and specialty medicines.This shift is crucial because these products command the highest prices and represent the fastest-growing segments of the global market. By localizing their production, the Kingdom captures the maximum value from its pharmaceutical spend.

Simplified Regulatory Pathway — The SFDA is working to streamline and accelerate the approval process for locally manufactured drugs and biosimilars, a clear incentive to reduce time-to-market for companies that choose to comply with the localization strategy.

The Gulf Biotech Triangle: Competition and Synergy

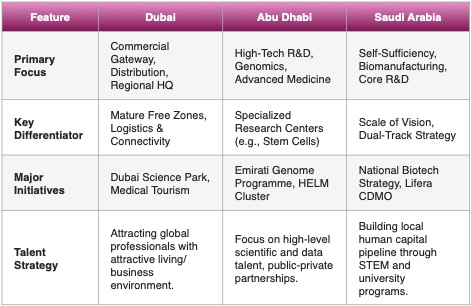

In our previous articles, we already discussed the overall strategies of Dubai and Abu Dhabi. The pursuit of leadership in the global biotechnology and life sciences sector led by Saudi Arabia, Abu Dhabi, and Dubai has become a cornerstone of economic diversification across the Gulf Cooperation Council (GCC). Although all three jurisdictions aim to attract significant foreign direct investment and high-value talent, their execution strategies specialize in different segments of the biotech value chain. Saudi Arabia’s approach is fundamentally industrial and driven by a mandate for sovereign drug security, focusing heavily on localization and foundational bio-manufacturing. Abu Dhabi is strategically building a highly integrated innovation vertical, concentrating on data-driven health, artificial intelligence (AI), and complex research and development. Conversely, Dubai leverages its established prowess as a global logistics and commercial gateway, prioritizing the attraction of regional corporate headquarters and facilitating rapid commercialization through specialized free zones.

We have compared the strategic goals of these three jurisdictions in the following table:

The Competition: The Fight for the Gold

To realize their strategic goals, the primary tension among these three jurisdiction is the battle for corporate headquarters and elite talent. Dubai vs. Saudi Arabia: This is the fight for the Regional HQ crown. Dubai, the established Global Host, offers sophisticated free zones and logistics. Saudi Arabia, the Challenger, uses its massive market size and state contracts (Vision 2030) to mandate that foreign firms relocate their regional HQs to Riyadh, directly challenging Dubai’s commercial dominance.

The Talent Scramble: All three are engaged in a Gold Rush to attract the same finite pool of world-class scientists and capital, offering escalating incentives to secure the best minds.

The Complementation: Three Pieces, One Puzzle

Despite the rivalry, their focus areas allow them to fit together, covering the entire biotech product lifecycle—from lab bench to patient delivery: A product is Discovered and Designed in Abu Dhabi’s research centers, then Mass-Produced by Saudi Arabia’s manufacturing scale, and finally Distributed across the MENA region via Dubai’s logistics channels.

In essence, Dubai is the commercializer, Abu Dhabi is the specialized innovator, and Saudi Arabia is the national champion pursuing both manufacturing scale and fundamental research depth simultaneously to achieve complete health sovereignty. While they compete fiercely for global recognition and investment, their specialized strategies create a powerful, complementary regional value chain. This Biotech Triangle ensures that the entire lifecycle, from research and development to commercialization and distribution, can be completed within the GCC region.

Future Outlook of MENA Biotech Triangle (2026 - 2030)

The biotech outlook for the GCC’s “Biotech Triangle” over the next five years is characterized by accelerated, AI-driven growth amid intense strategic competition. Specialized roles are solidifying: Abu Dhabi will likely lead the AI-enhanced R&D and precision medicine (the Innovation Engine), Saudi Arabia will dominate large-scale, optimized biomanufacturing (the Production Powerhouse for health sovereignty), and Dubai will retain its role as the primary Commercial Gateway and logistics hub. Geopolitical factors reinforce the need for localized production, anchoring Saudi Arabia’s self-sufficiency drive. While competition for HQs will increase—forcing some bifurcation between Riyadh and Dubai—the complementary nature of the three hubs, powered by massive sovereign investment and AI/ML, ensures the rapid development of a complete, resilient regional value chain for MENA.

Disclaimer:

The information provided in this article is for general informational and educational purposes only. It is not intended as, and should not be construed as, professional business, legal, investment, or medical advice. Before making any strategic decisions, you should consult with a qualified professional. Calxera makes no representation or warranty of any kind, express or implied, regarding the accuracy, adequacy, validity, reliability, availability, or completeness of any information on this site.