A Baroque Crescendo in European Biotech Funding in 2025

October 06, 2025

This week, we’re going to take a closer look at the Europe biotech funding activities in the first three quarter of 2025.

This year, European biotech fund-raising landscape has proven its resilience, with significant capital flowing into the sector despite broader economic headwinds. While the overall number of deals may be down, the industry has seen a clear shift toward larger, more selective investments. This new reality is defined by megadeals for companies with a clear path to market and a focus on cutting-edge technologies like AI and highly sought-after therapeutic areas.

Changes in Fundraising Trends

We notice that the fundraising landscape in European biotech has undergone a notable shift when comparing 2025 to the 2023-2024 period:

Rise of Megarounds: While overall deal volume and the number of deals may have fluctuated, the presence of multi-hundred-million-dollar “megarounds” for a select few companies has become a dominant feature in 2025. This contrasts with 2023, which was characterized as a “year of retrenchment” with a more defensive posture from investors.

Focus on AI and Specific Therapeutic Areas: A significant amount of capital has been directed toward AI-driven drug discovery companies and those working on therapies for highly lucrative and in-demand fields like obesity. This trend was gaining momentum in 2024 but has accelerated in 2025, highlighting a clear investor preference for disruptive technology and high-growth markets.

Increased Investor Selectivity: After the broad investment patterns of the pandemic-era (2020-2021) and the subsequent “reset” in 2023, investors have become more cautious and strategic. The funding is no longer spread thin across numerous early-stage ventures. Instead, capital is being deployed selectively into companies with mature pipelines, validated technology, and a clear path to commercialization. This is evidenced by a higher median deal value for companies with drugs in later clinical stages.

Subdued Public Markets: The IPO market for European biotechs remains challenging, continuing a trend from 2023 and 2024. With few companies successfully going public, private funding, particularly large VC rounds, has become the primary mechanism for companies to raise significant capital. This continued stagnation in public markets makes the large private rounds even more critical for the sector’s growth.

egional Shifts: hile the UK continues to be a leader in the European biotech space, other regions like DACH (Germany, Austria, and Switzerland) have seen an increased share of the total capital raised, a notable shift from previous years.

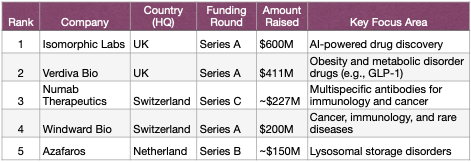

Top 5 Biggest European Biotech Funding Rounds (as of September 2025, based on public data)

Summary

Overall, 2025 has been a year of strategic consolidation for European biotech funding. The market is maturing, with investors increasingly favoring large, impactful bets on companies with strong data and disruptive technology, particularly in the AI and metabolic health spaces. This trend suggests a flight to quality and a focus on de-risked assets, a significant shift from the broader investment patterns of previous years.

Disclaimer:

The information provided in this article is for general informational and educational purposes only. It is not intended as, and should not be construed as, professional business, legal, investment, or medical advice. Before making any strategic decisions, you should consult with a qualified professional. Calxera makes no representation or warranty of any kind, express or implied, regarding the accuracy, adequacy, validity, reliability, availability, or completeness of any information on this site.